Through Executive Decree No. 356 of April 7, 2026, published on April 8, 2026, in the Third Supplement of the Official Register No. 260, the General Regulation of the Public Procurement Law (“RGLOSNCP”) was amended.

Below is a summary of the amendments:

- Sanctions for suppliers. The infractions established in article 119 of the Public Procurement Law (“LOSNCP”) must be sanctioned by the National Public Procurement Service (“SERCOP”) with the suspension of the offender’s Single Registry of Suppliers (“RUP”). For the imposition of this sanction, SERCOP shall apply the following grading:

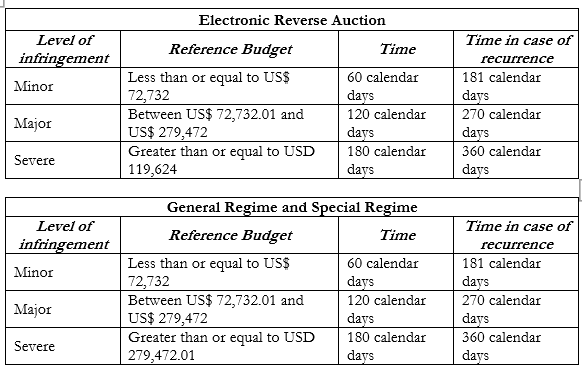

1.1. The infractions defined in literals a) and c) of article 120 of the LOSNCP (e.g., providing false information or links between bidders, respectively) are sanctioned considering the reference budget and the public procurement procedure in which the infraction was committed, as explained below:

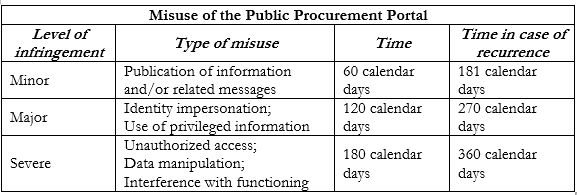

1.2. The infraction defined in literal b) of article 119 of the LOSNCP, which relates to the types of misuse of the Public Procurement Portal established in article 25 of the RGLOSNCP, will be sanctioned as explained below:

1.3. The infraction defined in literal d) of article 119 of the LOSNCP, related to the commission of acts of dishonesty during the certification of operators of the National Public Procurement System, will be sanctioned with a 180-day suspension of the RUP. Additionally, SERCOP may annul the irregularly obtained certification.

- Claims before SERCOP. Bidders’ claims filed before SERCOP in accordance with Article 115 of the LOSNCP, regarding unlawful actions by contracting entities during the pre-contractual stage, must be resolved within a maximum of 15 business days, counted from the date the contracting entity submits its rebuttal or from the expiration of the deadline to do so, if no response has been submitted. Article 433 of the RGLOSNCP explicitly established that failure to comply with this deadline resulted in SERCOP’s loss of competence to resolve the claim. Following the reforms, this provision was removed; however, contracting entities are still authorized to continue with the procurement process even without a decision from SERCOP. This creates a legal gap that SERCOP must address.

- Central Bank of Ecuador (“BCE”). Under the special regime of Article 149 of the RLOSNCP, the BCE can contract directly and, if necessary, under reserve, non-cataloged strategic goods and services for the operation, security, and sustainability of the financial system, including: external audit, management of valuables, coin minting, financial infrastructure, gold management, and technical systems for stability and prevention of money laundering.

Xavier Rosales, Partner at CorralRosales

xrosales@corralrosales.com

+593 2 2544144

Hugo Garcia Larriva, Partner at CorralRosales

hgarcia@corralrosales.com

+593 2 2544144